Extending the "Exist"ense!

Extending the "Exist"ense!

Fiscal that is Monetary!

NIFTY

FOMC blues gets over, Global Markets continue to Fight the FED. Holding still hopes for larger cuts. There is something that needs to give in.

The growing concern on the exposure to real estates, the credit exposure and the market to market are driving the narratives. Are we closer to any credit event, if so will that also pass the test.

Japan Bank Aozora, tanks, on disclosure of exposure to US Commerical Real Estate. Are there more to come? Similar concerns have been raised in Canada Real Estate, but much of the movements have not disturbed the broader markets.

Today JOBS data is crucial as any softer data if any, will push the probability of Rate cuts more, despite FED declining not a possibility in March. Financial conditions continue to remain easy.

Our budget, thankfully, remained balanced, focus more on extending the current measures, than anything new. In any case this is Vote on Account budget. The surprise is the broader relative lower borrowing, that pushed the yields lower, markets cheer, in any case that is a discussion from the actual budget. For now, latch the positives.

Mixed data from Asia, focus is on US data and Michigan Consumer Sentiment Final/inflation expectations.

From the Technical perspective, bulls holding the gains and almost near the upper end of the range, a close above 21830 opens the scope for ATH, the probability growing, that is part of the larger structure, one more high one more failure, the net benefit is the higher base, rotation on the sectors that is the theme that continue to unfold.

Bear's need a close below 21630 while bulls work towards the 21850-900 being weekend and important data, ideally this level to hold.

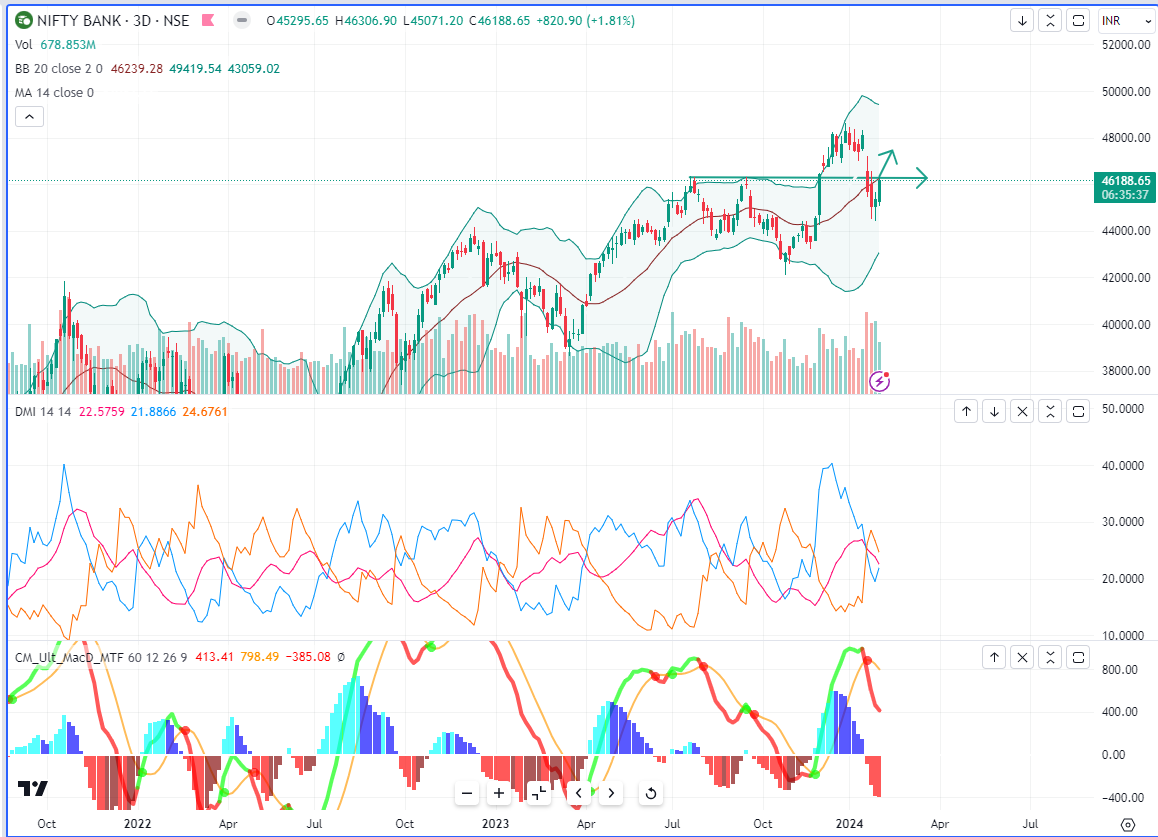

NIFTYBANK

Concerns as expected remained localised, focus shifts to the budget and post FOMC market moves.

Crude cools, surprise remains from the budget on fiscal deficit towards the 5.1%, that is huge positive, relatively lesser and lower cost of borrowing projection, market cheers yield falls, the major beneficiary the PSU banks rally. What unfolds later is the year end taking, for now that is enough to build the base.

The fall towards 44600 slowly turning out to be the base, ideally today action should settle for move towards the 47000 and probably higher.

US jobs data remains one more piece of information, without troubling much. The good part of the Bank Nifty is the larger members, more so the PSU bank continue to print to the North, the heavy weights have reasonable hit some short term pause to push.

23 Jan high is one area of supply while 47000 is larger area of resistance. Supports move to 45600-700 area for move higher.