Search for "Neutral"

Search for "Neutral"

Removing "Sound" from the Banking.

NIFTY

Volatility is the name of the game. In the bottom and top formation, it is the fight for the top of bottom that brings in volatility.

The question is what is triggering the volatility, is it underlying economy, socio factors, politics or the geo-political or the combo of all. Search for the middle or needle that is moving all of them is vital.

Talk of Middle or Neutral, Powell in his press conference clearly says, no one knows what neutral rate is, so please stop searching for neutral, pivot or any such rhymes.

Look at this on Monthly Close, NIKKI takes the max on the up move, Next Comes Dow and SPX (1.5% kind of), Asia other than Japan all are red or token green or token red. Ditto NIFTY just -5.7 points, while the high and low are near 1000 points. Welcome to the world of 2024, where men's and boys are separated.

The economic data is reasonably good or appears to be good. Europe average economic data points to no growth, so technical or no technical, calls for recession are mature to premature. The end result is the yield gap between Europe and US now gets narrowed, result the Dollar Rally.

Two African Countries are in currency turmoil, Egypt and Zambia, not any trigger. While the New York Community bank, issues push the safe heaven on the Treasuries. Despite ruling the rate cut in March, Gold has been steady and that is a point to take away.

From the attached graph out of the last Six Days the net action is Nil, while we have three Red Candles and Three Green Candles, no need to emphasis the NET aggregate size of all the three are NIL.

In terms of larger degree this month action remains important like any other month, volatility remains the name of the game.

From the internals, we are at we are best at. Neither side looks strong or week. Next move is important to get the clue. Stand Alone looks buy lower, cues suggest sell higher. Pick your side and size and seize the moves.

Larger range 21450-21850, squeeze 21630-21780

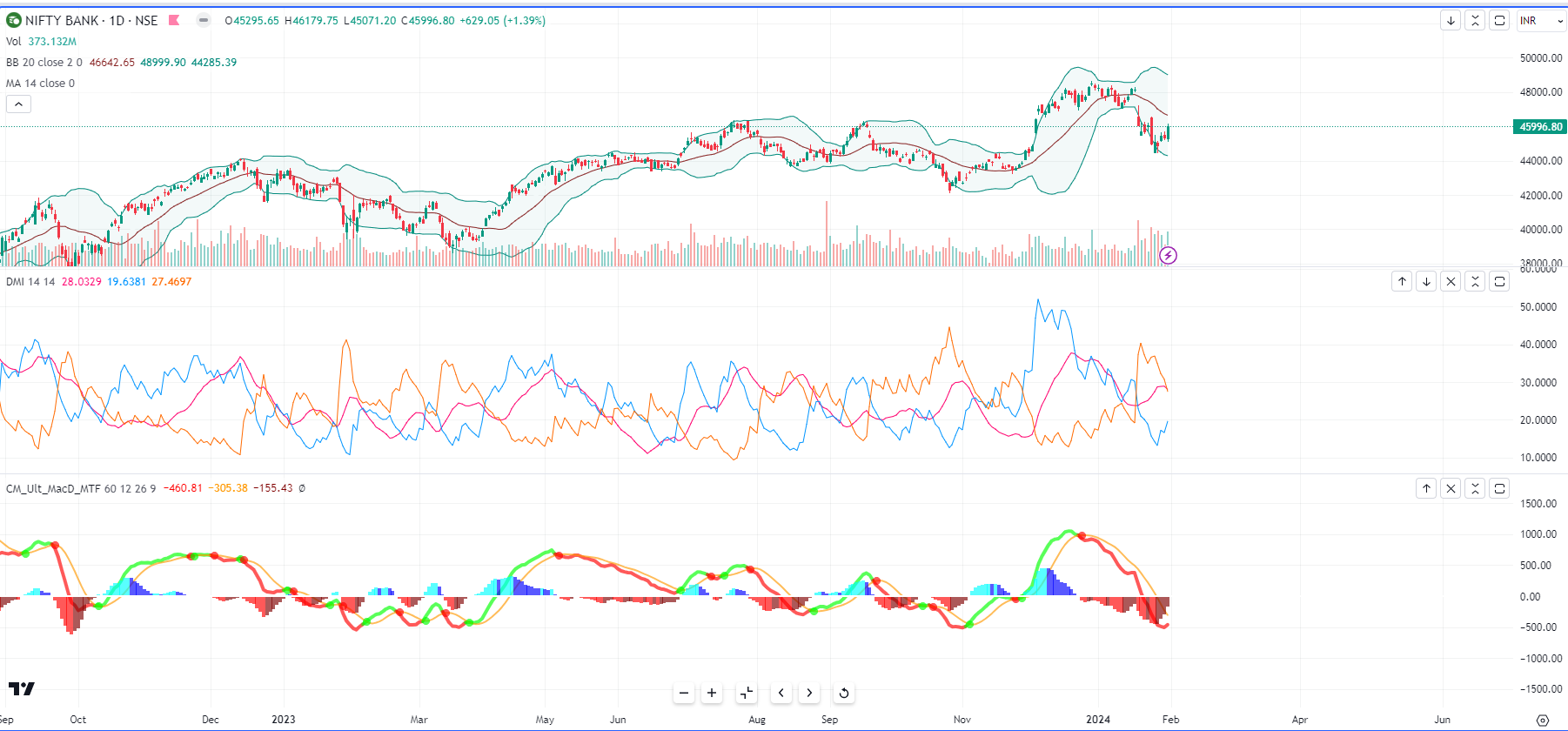

NIFTYBANK

Notable from the FED Minutes is the removal of the Sound Banking Systems on a day when the NY Community bank issues surface. The question is, is there a question on Banking System Soundness or at least the financial systems.

Locally, the RBI Circular on the 97 Communications (Paytm), sends lots of concerns to the market participants, not on why, but what is the real issues behind the circular. Uneasy remains the theme. NBFC are wobbling, we have seen the BAJAJ Twins, we witnessed the AU Small Bank tanking. The only resort looks to be the PSU Pack, the mean reversion is very active here.

The FED cuts are behind, now not even in March. The very high hopes of Six rate cuts, one Quarter of forecasting is done and dusted at least for now. China Caixin PMI comes above expectation, but not the Chinese Markets.

Asia cues are mixed, we have our own budget, despite no expectations, expectations still run high. Our PMI is due almost one hour into the market, but focus is the budge if any surprises than any prizes.

Issues surrounding the PAYTM can be some clues, but it would be more localised and orderly than otherwise.

New month, new hopes and old tricks and Old Range.

Big Range is 44600-466600. We are near the 46000 so shorter-range squeeze is 45600-46400.

The monthly candle is bearish engulfing, and sectoral this one closed as and almost where it was in July 2023 (start). The banking sectoral funds are near zero return last 7 months, thanks to HDFC.

For the bull's action is in PSU space, for the bears Private Banks selective and Old Private Sector of the Financials on sell higher mode.