"Stranded" Asset!

NIFTY

UBS in its weekly blog writes about Stranded asset. It is an asset that loses its value earlier than expected. The main causes range from change in underlying economic structures, innovation and revolution making the previous ideas into liabilities.

The I told you, so story is more on the face in terms of financial assets forecasting than ever. When Auto Rickshaw driver performance, exceeds the Quant Funds performance, it is time to think than "Tinker".

The last two decades have been one of buy hold get rich stories, it will feed in itself all one has to do is sit tight to get right. That surely is undergoing a silent change. Sooner one sees the better. The great exit of 97 Communications (Paytm) by Warren Buffet can be a case in point.

The stranded asset range from education to real estate opines the author, Paul Donovan. Interest read.

Clearly less is more, is the realisation, move over from diversification focus on a few that can hold the ideas together.

Jobs data from US hits the face of the camp that went on gungo in terms of six plus rate cuts. The majority or the so-called Consensus trade, remains on the thin edge. It remains the ritual of the recent decade. Dollar bulls roar and stay above the 104 handle. With the near consensus of rate cuts in Europe and UK, no rate hikes in Japan or China, it is clear that the Dollar will remain to rule. More gains are sure to hurt, but that is what it is. Powell suggests three cuts, against market expectation of six cuts plus.

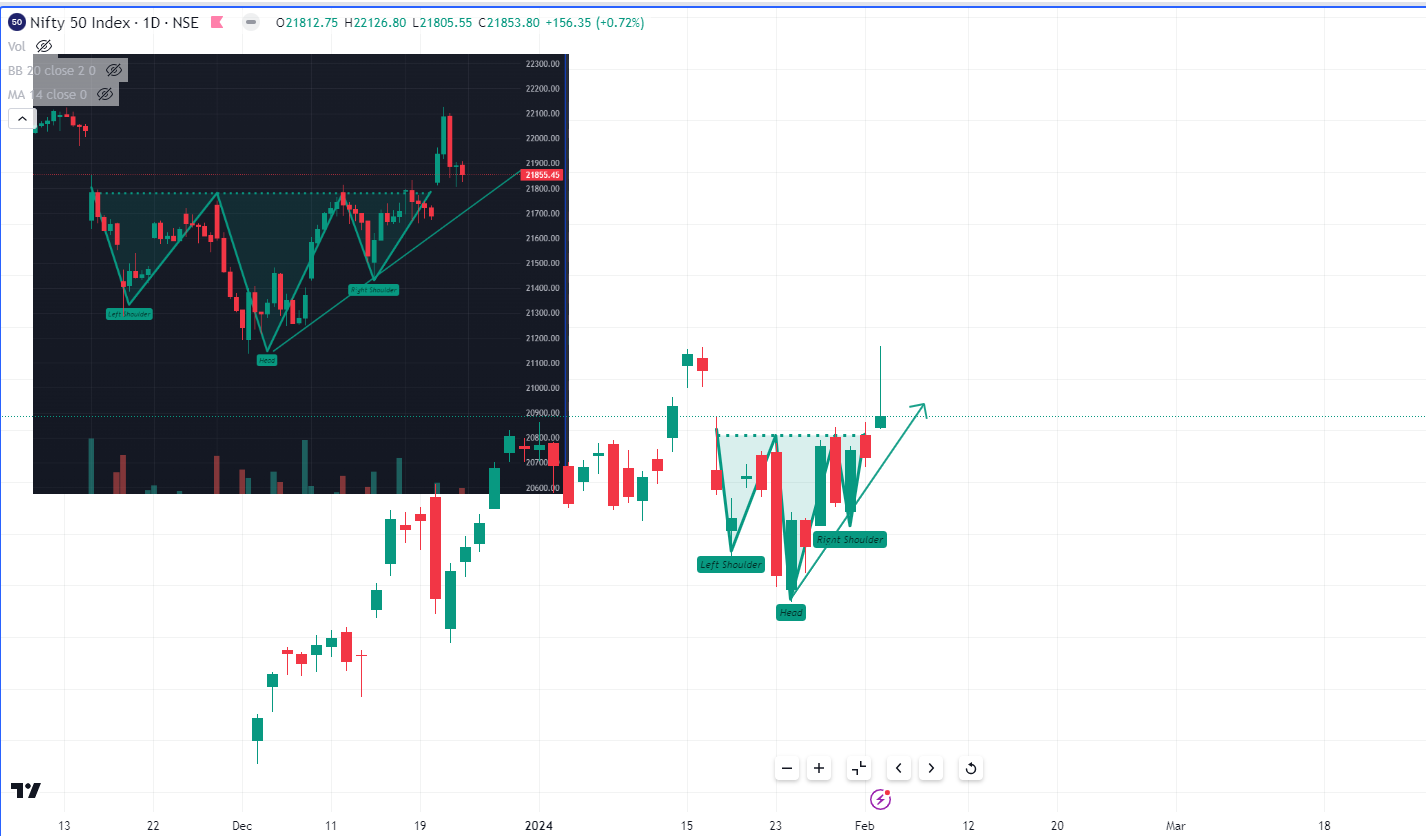

Back to NIFTY. Interest or worrying to note the Friday Candle posting the Gravestone Doji. Clearly the top looks heavy. Are we going to witness the China cheaper other EM more so the India as expensive story to unfold for some time?

The PIP graph is intra-day the inv head and shoulder break met very strong bearish engulfing pattern. If we close below the 21780 or if we loose the 17650 then the dice is towards the recent low than ATH.

Suggest shorts stops 21930 for move towards 21550 (may not be a day's job)

NIFTYBANK

Large players in the respective field have been in the eye of the market movers. They range from HDFC HLL to PAYTM.

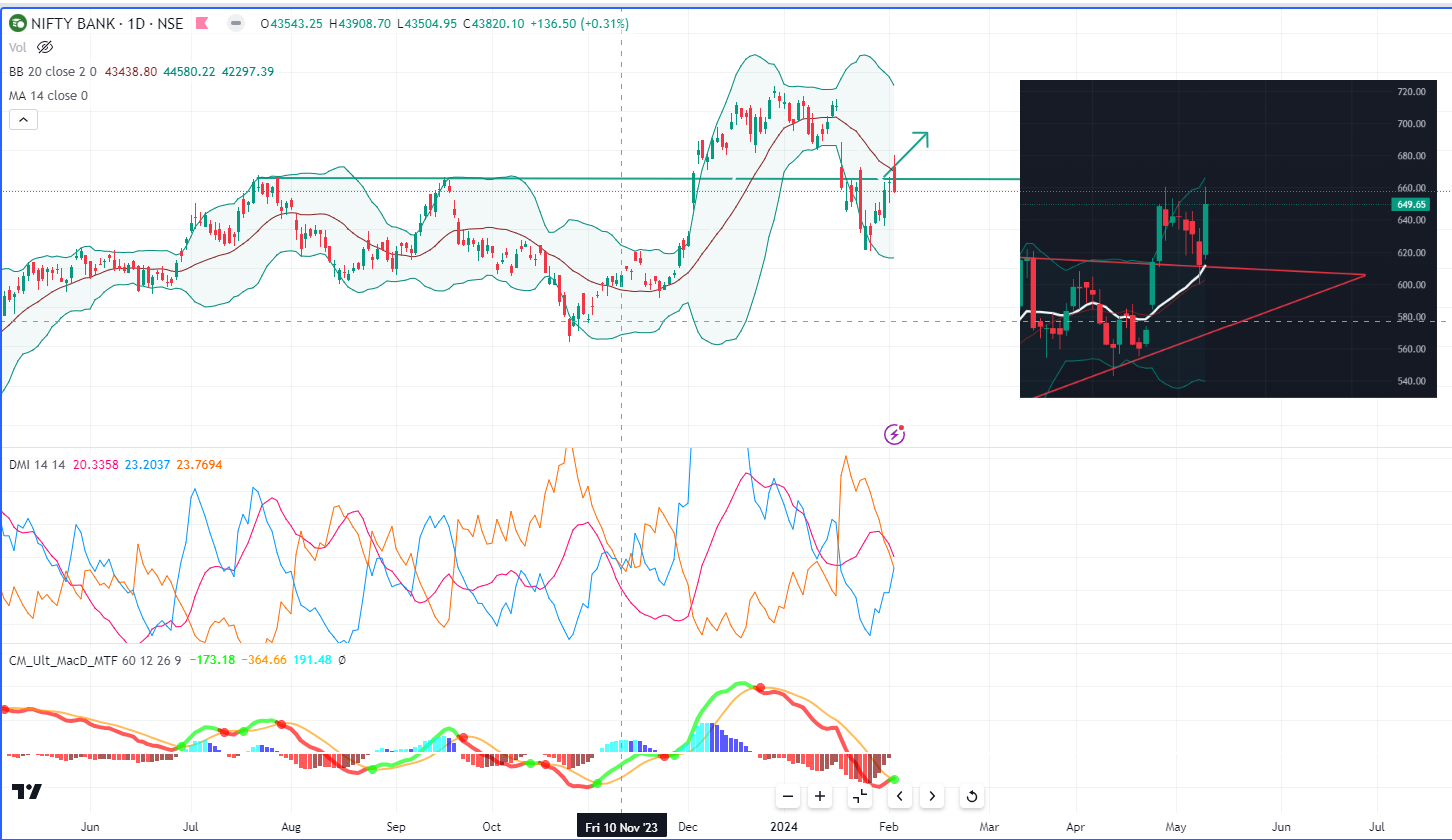

SBI results were out during the weekend. Provisions from the Pension surely a premptive and one off. There are areas of decline, but NIM of 300 plus on a large Balance Sheet size is not a simple to hold. Comparision galore with HDFC, they stay at the bank till the market opens.

Vision Pro release from the Apple, gets the required excitement but the pricy tag can hold the idea of owning at bay for many. Or will it be EMI life that can drive this too.

The fall of BANKNIFTY on Friday from the crucial level is a worry in point. With the SBI mixed view to start can add. However, the stand-alone graph of SBI (IN PIP) suggests these falls are an opportunity. 1) The PSU pack continues to rule, more so the less liquid spaces 2) SBI has not relatively moved up much it is more or less in 600-680 range. One can further squeeze the base to 640.

Elsewhere, the Dollar Rise, the Yields gallop, the inflation path remains to the north. (Inflation is still rising and the prices what we pay relative to last year is still higher, it is only the rate that is stabilising, even that is not assured now and is in steady ascent)

Clearly the rising USD Yields, and continued uncertainty in the larger names can dampen the Index, while the PSU Pack remains on to further gains.

Direct break below 45700 punctures the up move and opens one more attempt towards the 44800-45000. Larger Range 45400-46400 within that 45700-46200