"The Floor Test"

NIFTY

The Friday moves from the Index does not reflect the underly belly volatile moves beneath.

PSU Pack gets hammered, that is where the maximum interest has been in the recent times.

Very short term most of the sectors looks softer save a bottom move in Nifty bank (nothing guaranteed yet and Pharma sector. Here too selective rule the roost.

NIFTY ENERGY n Metals appear short term corrective path. Consumption remains the weak link in addition to MNC/FMCG.

In terms of leadership role, we had RIL SBI ONGC TCS played the part. In addition to other PSU Pack. One has to see how much this can sustain.

The Gift Nifty cues are near 80 plus but that is on weak footing as the volumes there are not sufficient indicator. In otherwards the first hour action remains the cue.

On a absolute basis, we have not moved anywhere since Dec 18 that is almost near two months, while the volatility remains at heightened activity. Clearly the nimble and humble game at play. The buyer and seller of the options market also feeling the same heat.

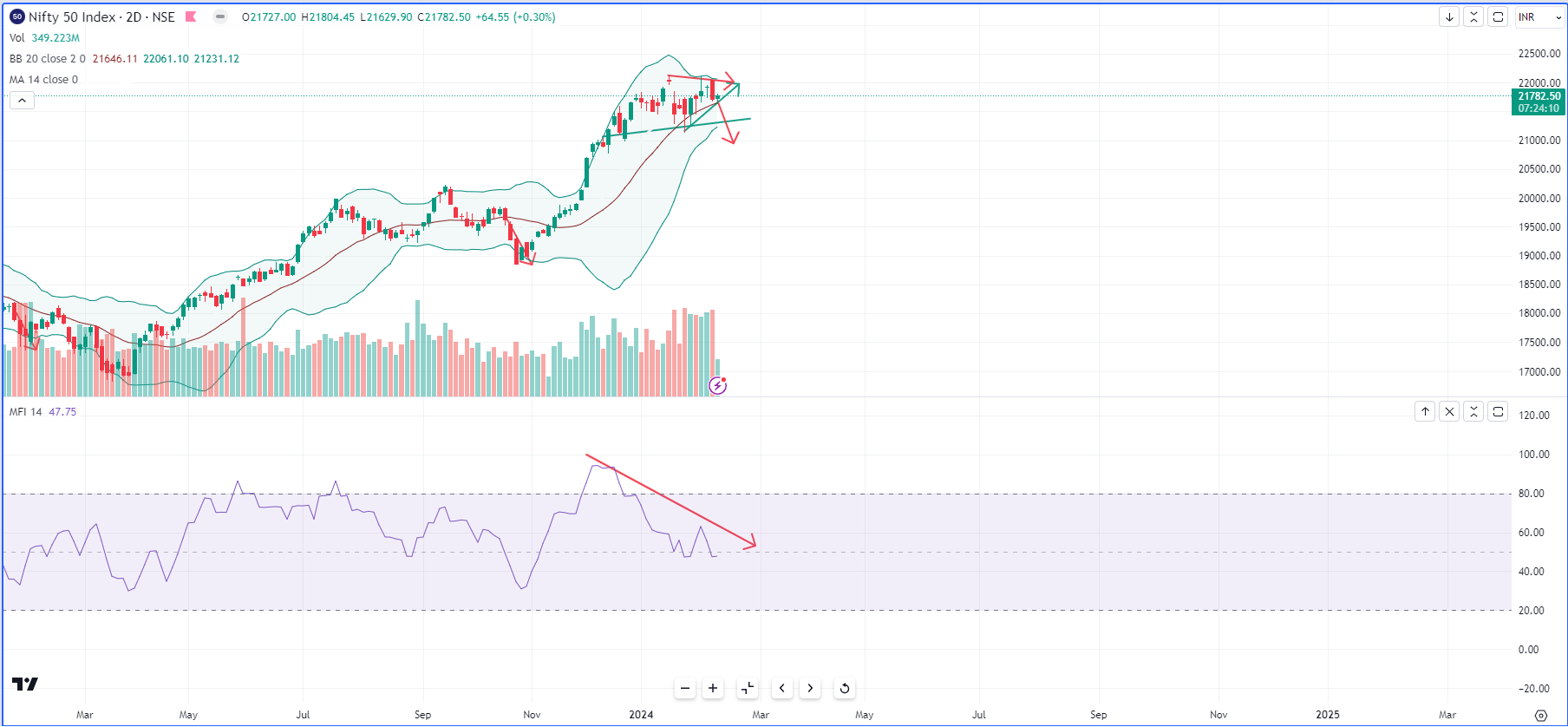

Repeated attempts to close below the 21630-680 failed, that gives hope to the up-move. This is the floor that the bulls have to keep in mind if they have to make any meaningful rally.

The Money Flow indicator suggesting, there is lack of interest to follow through, and the probability of failure at higher area is more than the failure at the lower end.

One factor that one has to keep in mind is the Floor test in the Bihar Assembly. With so much of the drama, any negative outcome there, markets would punch down heavily, while the positive outcome may not give enough rally.

One can blame it on Stars Mars aligns with Pluto at zero degree on 14 or Mars conjunct Pluto at 5-degree Capricorn on 13 February. All these indicatives of heightened concerns on the Governments across the world.

Later after close, our Industrial Production and Inflation. Later in the Week US inflation numbers. Overseas cues have been mixed. Year of the Dragon holidays in China, so nothing much to borrow from there.

While below 21880-930 are or if we open closer to 21900 allow 22050 as the stop for move back to the day's low. A direct break below 21630 pushes deeper moves down.

NIFTYBANK

Interest rates on EPF have been one indicator of the markets in previous cycles to foresee the path. For, these rates are an indication that the path of the rate is much more stable in the direction of the action. This time increase.

We are back to where we were nearly a decade plus.

US CPI revised one comes unchanged, takes some sting out of the worries, but the job is still not done yet is the conclusion. This inference, echoed by our RBI Governor in the Policy assessment.

RBZ ready to hike, Turkey another one which is embarking on hikes with the change in the CB Governor. US Yields and US Dollar both on the higher trajectory. No China as year of the Dragoon holidays.

Bull or bear depends on which frame one is looking at the Index. The bi-monthly frames posts that the bears are not done yet, and the next couple of weeks is crucial, an indicator volatile range remains the conclusion.

Bulles need quick close above 46300 to reassert. While bears are trying an failed attempt towards the mid 44 K.

It is difficult to see NIFTY down, when NIFTYBANK shows short term strength or vice versa, unless it is aided by other heavy indexes like Energy IT or the Metal or the combination.

Today would be one such day to watch. Industrial production and inflation data due after market close. Vital the political front any unexpected developments.

Inclined to clip around 45200-46400 range. Bias tad on the buy side though.